Pages

1

To the Honorable Finance Committee of the City Council of the City of Fort Worth. Gentlemen.

Attached hereto you will find a letter from Henry C. Scott, President of the Fort Worth Light and Power Co. with whom I have had some conversation relative to the appeal taken by said Light and Power CO. from the valuation placed by the Board of Equalization upon the personal property of the said Company.

I feel that the matter is one for your consideration in connection with my opinion on the subject which I hereto attach. If the case were one in which it were possible to settle the principles as to whether or not the intangible property of a corporation could be assessed for taxes by an indirect process as it may be called, I should cheerfully proceed to litigate the question even though I believed that I should be beaten as I deem it very advisable to have settled once for all the question aforesaid. That question in my opinion cannot arise in this case, and the very best that could be done would be to litigate over the actual value of the property listed by the Light and Power Co. as personal property. So far I have been unable to learn that we will be able to prove a greater value for the said property as personal property than the valuation placed upon it by the Company.

I should not have felt called upon to refer this matter to you had it not been for my views of the law as expressed in the accompanying opinion and for the feeling that I have that it is not well for the city to enter into a course of litigation with the chances so largely against it when the trouble which produces the situation can be so easily remedied upon another assessment. If you gentlemen should feel called upon to present this question to the Council I shall be most happy to follow the directions that may be given me either by you as a committee or by the Council as a body.

Very respectfully, ECOrrick City - Atty

2

HENRY C. SCOTT, President. 421 Olive Street, St. Louis, Mo. F. B. HARROLD, Vice-President.

SAMUEL BECK, Secretary. J. C. LORD, Superintendent and Engineer.

● ● OFFICE OF ● ● The Fort Worth Light and Power 809 Houston Street, Dundee Block.

Fort Worth, Texas, Nov. 24th 1903

Hon. E. C. Orrick, City Atty., Fort Worth, Tex.

Dear Sir:

Referring to the controversy between the City of Fort Worth and this Company, respecting the assessed valuations put upon our personal property, we propose, for the purpose of bringing the matter to a speedy and amicable settlement, to pay the personal taxes assessed against us for 1902, although the assessment is in our view irregular and excessive, and will pay personal taxes for 1903 upon a basis of $83977.60 valuation, which represents the true value of our personal property.

This basis of settlement, although much above what we should pay, we propose as a means of ending an unfortunate and regrettable controversy with the City, for we will thus pay or will have paid all real estate taxes assessed against us, and the personal taxes as above, and will have thus fully met our share of the burden put upon those who must take care of the City's annual requirements.

Yours truly Henry C. Scott

3

To the Honorable Finance Committee of the City of Fort Worth.

Gentlemen.

An appeal has been taken by the Fort Worth Light and Power Company from the valuation placed on their personal property by the Board of Equalization of the city of Fort Worth and in pursuance of my duty it devolves upon me on behalf of the city of Fort Worth to attempt to sustain the valuation placed upon the said property by the Board of Equalization.

The Power Company rendered their property to the City Assessor and Collector specifying each item of what it termed its property and what is termed personal property in the assessment in which was included its wires, its poles, its machinery and such like together with its horses, carts, wagon, office fixtures and merchandise.

With reference to the property as rendered I understand that the contention of the Board of Equalization was that as a property this property so rendered was more valuable than rendered by the company and possibly that the items themselves were worth more money than the value placed upon them by the company. Considering it from a legal standpoint the assessor having assessed the property of the Gas Co. be so assessed as to in effect compel the Gas Co. to pay a tax on its franchise, that is its easement in the streets, as distinguished from the franchise granted by the state, to-wit its charter, and if so how can this be done and can it be done in the manner attempted. A very careful consideration of the question in the light of the authorities upon the subject in the state of Texas convinces me, first, that a public corporation such as the Gas Co. having rights granted to it by the public be made to pay upon the value of such rights, but under our charter the method of requiring such payment must necessarily be the inclusion of such value in the valuation of the real estate of the corporation. The question then arises as to whether or not, not only the franchise as the term is heretofore used, must be considered as real estate, but with the property listed by the assessor as aforesaid is real or personal property. Under our charter and the authorities upon the subject there can hardly be any doubt that the great bulk of the property of the Gas Co., I might say all of it with the

4

-2-

exception of a few thousand dollars worth , is real estate.

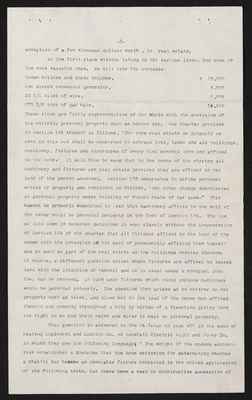

In the first place without taking up the various items, but some of the more valuable ones. We will take for instance:

| Seven boilers and three engines, | $15,000 |

| One direct connected generator, | 5,600 |

| 23 1/2 miles of wire, | 3,875 |

| 773 3/5 tons of gas main, | 14,679 |

The question is answered in the 74 Texas on page 605 in the case of Keating Implement and Machine Co. vs Marshall Electric Light and Power Co. in which they use the following language: "The weight of the modern authorities establishes a doctrine that the true criterion for determining whether a chattel has become an immovable fixture consisted in the united application of the following tests. Has there been a real or constructive annexation of

5

-3-

the article in question to the realty? Third, whether or not it was the intention of the party making the annexation that the chattel should become a permanent accession to the freehold, this intention being inferable from the nature of the article, the relation and situation of the parties interested, the policy of the law in respect thereto, the mode of annexation and purpose or use which the annexation is made. And of these three tests pre-eminence is to be given to the question of intention to make the article a permanent accession to the freehold, while the others are chiefly of value as evidence to this intention." In this case as stated in the opinion the District Court held in effect that intervenor had a valid mortgage but that it did not give to it a proper lien against anything except the personal property of defendant, and that the poles, wires etc. erected in the streets were parts of the realty, and rendered judgment accordingly. After laying down the principles as aforesaid the Supreme Court affirmed the judgment of the District Court holding thereby directly the poles, wires etc. of the Electric Light Co. erected in the streets were parts of it realty.

It is laid down in Cooley on Taxation that the mains of the water plant are parts of its realty and I do not apprehend that if the question is pressed to a decision that there will be any question but that the courts will hold that for purposes of taxation that property of the character mentioned is as much a s part of the realty of the Gas Co. as the buildings erected over its machinery upon its land.

The case of the State vs the Austin and Northwestern Ry. Co. in the 62 S. W. 1050 being the celebrated case in which the question of the right of the said state and county to assess and collect franchise tax was determined, reads as follows in so far as it bears upon this question. "Art. 5062 provides that real property for the purposes of taxation shall be construed to include the land itself whether laid out in town lots or otherwise and all the buildings, structures, improvements or other fixtures of whatsoever kind thereon and all the rights and privileges belonging or in anywise appertaining thereto and all mines, minerals, quarries and fossils in and under the same." It seems to us the plain purpose of the article quoted to require that in assessing real estate for taxation, whether held by a natural person or a corporation, there shall not only be included in the valuation the value of the land itself merely as land together with the im-